The official federal budget process currently in statute was established by the Congressional Budget and Impoundment Control Act of 1974. The Act outlined a structure and timeline to more formally coordinate lawmakers’ crafting of the federal budget. However, the legislation did not enact enforcement mechanisms – there are no consequences for failure to meet deadlines or circumventing the outlined process.

The budget process begins in February, when the president’s budget is scheduled for submission to Congress after discussions with federal department and agency leaders about their needs. The president’s budget is a detailed recommendation to the legislative branch, which under the Constitution has the “power of the purse” to make decisions about funding.

After the president has submitted the budget, the next major step for Congress is to draft and adopt a concurrent budget resolution by April 15th. Because the budget is a concurrent resolution rather than a joint resolution, it does not require the president’s signature – only a majority vote in both chambers of Congress. The budget resolution includes instructions that guide Congress in spending and tax decisions throughout the year. The resolution establishes how much revenue needs to be raised and how much should be spent, but leaves it up to congressional committees to determine how those targets will be met.

| The Budget Process Timeline, as detailed in the Congressional Budget Act | |

| On or before | Action to be Completed |

| First Monday in February | President submits his budget. |

| February 15 | Congressional Budget Office submits report on the economic and budget outlook to Budget Committees. |

| Not later than 6 weeks after President submits budget | Committees submit views and estimates to Budget Committees |

| April 1 | Senate Budget Committee reports concurrent resolution on the budget. |

| April 15 | Congress completes action on concurrent resolution on the budget. |

| May 15 | Annual appropriation bills may be considered in the House. |

| June 10 | House Appropriations Committee reports last annual appropriation bill. |

| June 15 | Congress completes action on reconciliation legislation. |

| June 30 | House completes action on annual appropriation bills. |

| October 1 | Fiscal year begins. |

In recent years, however, the budget process has repeatedly broken down. Lawmakers failed to pass a budget resolution on time in almost every fiscal year since the passage of the Congressional Budget and Impoundment Control Act in 1974. Fiscal year 1999 marked the first time since the introduction of the modern budget process that formal action on a budget resolution went incomplete. This began an all too frequent 21st century trend of Congress bucking the budget resolution process altogether. Lawmakers did not pass a resolution for each of the following fiscal years: 2003, 2005, 2007, 2011-2015, 2019-2020, and 2023-2024.

When Congress does not pass a budget resolution, it must resort to other, less formal, processes. In some years, the House and Senate have enacted a “deeming resolution” that: a) gives reference to or sets specific budgetary levels; and b) makes its provisions enforceable as if it were a budget resolution. Congress can also use chamber-based budgetary rules or discretionary spending caps to guide spending and revenue levels in the absence of a true budget resolution.

Regardless of the guiding mechanism used, Congress must then assemble 12 appropriations bills to fund the coming fiscal year’s “discretionary” spending budget. Each bill funds a different set of programs in the federal budget (ex. Labor, Health and Human Services, and Education; or Homeland Security). According to the Congressional Budget Act schedule, these should be completed by June 30th, which had been the end of the federal fiscal year prior to the passage of the 1974 Act. The Act then moved the beginning of the federal fiscal year to October 1st, thinking that this should give Congress ample time to complete a budget; however, Congress has instead largely ignored these deadlines and struggled to pass bills by September 30th, the new end of the federal fiscal year.

Appropriations bills must pass by a majority vote in the House of Representatives and overcome the Senate “filibuster.” Under Senate rules, senators can keep debate open and delay or prevent votes on legislation by using the filibuster. To close debate in the Senate and overcome the filibuster, the chamber must reach a three fifths, or 60-vote, majority. This high voting threshold means that appropriations bills almost always necessitate bipartisan negotiations. Once the 12 bills have passed both chambers, the President’s signature enacts the federal government’s discretionary budget.

Discretionary and Mandatory Spending in the Budget Process

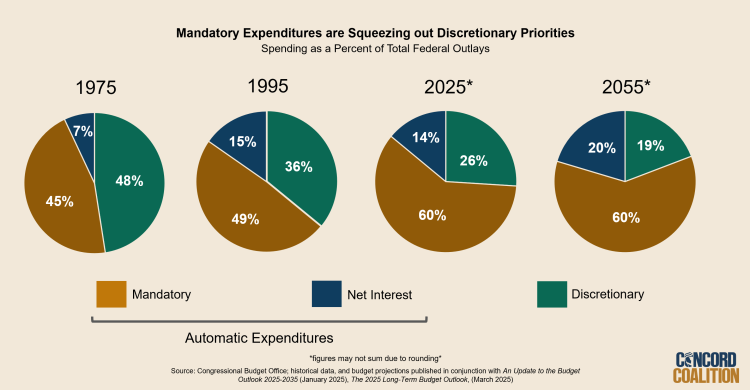

Despite taking up the lion’s share of the budget process, today, discretionary spending actually comprises only about a quarter of the federal budget. The standard appropriations bills include funding for spending categories such as national defense, law enforcement, the judicial system, the environment, education, medical research and transportation. When the Congressional Budget Act originally passed, discretionary spending was larger than mandatory spending, excluding net interest.

Spending on entitlement programs like Social Security and Medicare is known as “mandatory spending.” These programs’ expenditures are set by formulas which can only be adjusted by amending the law authorizing the programs. If no action is taken, these programs continue operating on autopilot.

Changes to mandatory spending, including entitlement programs (with the exception of Social Security), can be fast-tracked through an important legislative vehicle known as “reconciliation.” Reconciliation can also include tax policy changes and is only available when a concurrent budget resolution has been adopted. The original Congressional Budget Act assumed that a reconciliation bill would move in tandem with the appropriations bills and “reconcile” mandatory spending and taxation with the discretionary spending programs and keep the budget in line with the budget resolution.

However, in recent years, reconciliation has become used largely to move large partisan spending or tax cut bills in the Senate because reconciliation bills cannot be filibustered and are protected by points of order, restricting the amendments that can be offered. In recent years reconciliation has been used to pass legislation that increases the deficit while the original intent was to bring the budget into balance by reducing the deficit.

If policymakers wish to increase mandatory spending or decrease revenues, such changes are subject to statutory pay-as-you-go rules, also known as PAYGO. These rules require lawmakers to offset most deficit-increasing legislation over the following five and ten fiscal years. However, Congress frequently, regardless of which party is in the majority, waives the requirements that they created.

What Happens If Congress Fails to Pass a Budget?

Almost 75% of federal spending is mandatory and is essentially not affected by failing to pass a budget. However, the remaining 25% of discretionary spending is funded across 12 appropriations bills. If Congress fails to fund a discretionary program through one of the appropriations bills by October 1st, that public service will technically shut down. If appropriations are not enacted by that point, lawmakers have two options: allow a government shutdown, or pass a “continuing resolution” (CR). CRs are temporary measures that continue to fund discretionary programs at the previous year’s levels. You can read more about government shutdowns here.

Unfortunately, continuing resolutions have become standard procedure on Capitol Hill. These temporary measures not only reflect the failures of the budget process, but they also create challenges for agencies seeking to plan and allocate resources for the long-term. The last time Congress passed all 12 appropriations bills on time was 1996.

Options for Budget Process Reform

Given how often the budget process breaks down, budget policy experts have proposed many options for reform. Some promising ideas include consequences for lawmakers when budget deadlines are not met, creating stronger and more comprehensive PAYGO requirements, only allowing reconciliation to be used to reduce the deficit, and biennial budgeting, which would create a two-year cycle that enables more long-term planning and oversight. Other ideas for reform have centered around finding new ways to subject taxes and mandatory spending to more frequent oversight and review.

Continue Reading