While much of America was riveted by the Speaker’s race in the U.S. House of Representatives this past week, some important budget-related news slipped by with little notice. First, President Biden submitted to Congress not one, but TWO supplemental appropriations requests totaling $161.8 billion. Second, the Department of Treasury released its official end-of-year accounting for FY 2023. Third, the Bureau of Economic Analysis (BEA) released its preliminary estimate of third quarter real gross domestic product (spoiler alert: it sizzled). In case you missed one or more, here’s a recap.

Biden Submits Two Supplemental Appropriations Requests

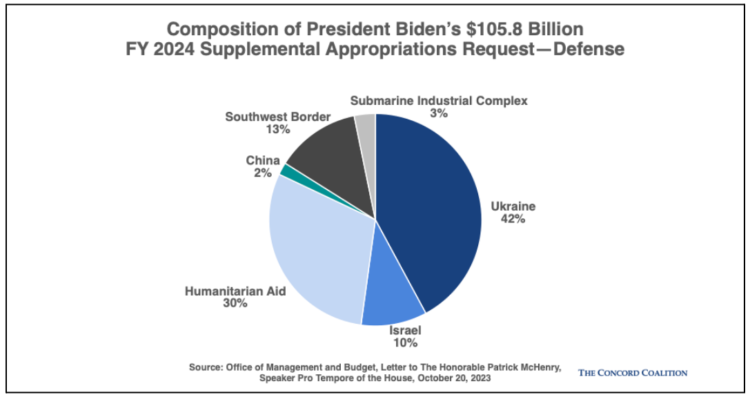

The geopolitical risks emanating from Hamas’ surprise attack on Israel October 7th injected new urgency and greater needs into President Biden’s supplemental spending request. The original $44 billion request—submitted in early August—was supplanted by a new $105.8 billion defense-related proposal.

In his official request to Congress, President Biden asked for $44.6 billion in military aid for Ukraine (purportedly sufficient for the entirety of FY 2024 which began October 1); $10.6 billion in military aid for Israel (largely for munitions and missile defense); $33.6 billion in humanitarian aid for Ukraine, Israel, and other Middle East nations affected by the crisis, and Indo-Pacific nations at risk to China aggression; $13.6 billion to enhance security and improve migrant processing at the Southwest border; $3.4 billion to support the U.S. nuclear submarine industrial base; and $2 billion in seed funding to aid developing nations and counter China’s rising influence in those regions.

While over half of the defense aid in this proposal is earmarked for Ukraine and Israel, a significant amount of that would be spent here in the U.S. to replenish domestic stockpiles of weapons, munitions, rockets, and missile defense systems sent abroad to defend those nations.

If President Biden has his way, this new supplemental funding would be designated as an emergency and would not count towards the FY 2024 spending caps agreed to in the July debt limit deal—nor would it be offset. It would be entirely debt-financed.

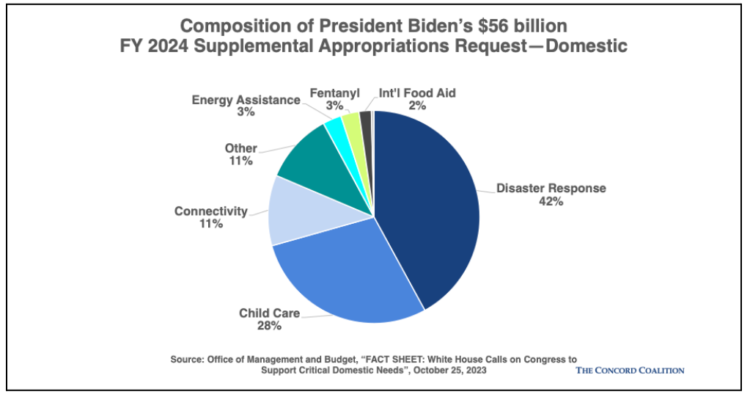

Five days after submitting his defense supplemental, President Biden asked Congress to consider a second FY 2024 request—a $56 billion domestic supplemental focused largely on priorities here at home: $23.5 billion for federal disaster relief programs, $16 billion for the extension of COVID-era childcare stabilization grants, $6 billion to extend high speed internet connectivity programs for low-income households, $1.6 billion in grant money for the Low Income Home Energy Assistance Program, and $1.5 billion to counter fentanyl abuse, and other priorities.

Like the defense-related supplemental, the new spending in this second request would be designated as an emergency and would be exempt from the FY 2024 discretionary spending caps. It would also be entirely debt-financed.

Concord’s assessment. It’s not unusual for a president to submit a supplemental spending request to Congress—it happens every year. But the sheer size of these two requests—a combined $161.8 billion—is stunning. Moreover, Congress has not yet completed the FY 2024 appropriations process (they’ve barely started) which means lawmakers have time to reduce allocations for the regular (base) appropriation bills to accommodate at least some of these urgent priorities. Pass a negotiated supplemental now, but offset at least some of its cost in the end-of-year omnibus (or whatever form the 12 regular appropriations bills take this year).

Treasury Releases Final Accounting for FY 2023

The Concord Coalition provided a sneak peek into the FY 2023 wrap up two weeks ago using data from the Congressional Budget Office, and the official picture from Treasury this week didn’t change our assessment much:

- The official deficit for FY 2023 totaled $1.695 trillion, but changes to the federal student loan program skew the budget data. After reversing FY 2022-2023 accounting entries for President Biden’s student loan forgiveness (which the U.S. Supreme Court declared unconstitutional), the actual deficit for FY 2023 was $2 trillion—$1 trillion more than FY 2022. The COVID emergency may be over, but the underlying long-term structural imbalance between spending and revenue remains.

- Revenues fell more than 9 percent in FY 2023. Part of this can be attributed to the unusually large (above trend) increase in income tax revenue in the prior year, but a combination of the FY 2017 tax cuts as well as several one-off factors (late and potentially fraudulent surge in COVID era Employee Retention Tax Credit claims, delayed tax filing for states affected by natural disasters, a drop-off in capital gains taxes, fewer purchases of foreign goods causing import duties to fall 20 percent, and a $106 billion reduction in Federal Reserve remittances) combined to produce an alarming drop in receipts this year.

- Net interest costs—the money the Treasury spends to service our national debt—jumped 39 percent, from $475 billion in FY 2022 to $659 billion in FY 2023. A combination of higher interest rates and $33 trillion accumulated debt make interest on the debt the fastest growing category of federal spending.

Concord’s assessment. Congress and the Biden Administration need a fiscal sustainability plan, but as of now they don’t even have a plan to fund the government past November 17th (when the continuing resolution expires). No matter how you count it, the final number for FY 2023 represents not just a failing fiscal policy but a failure of leadership.

Third Quarter GDP Growth Sizzles

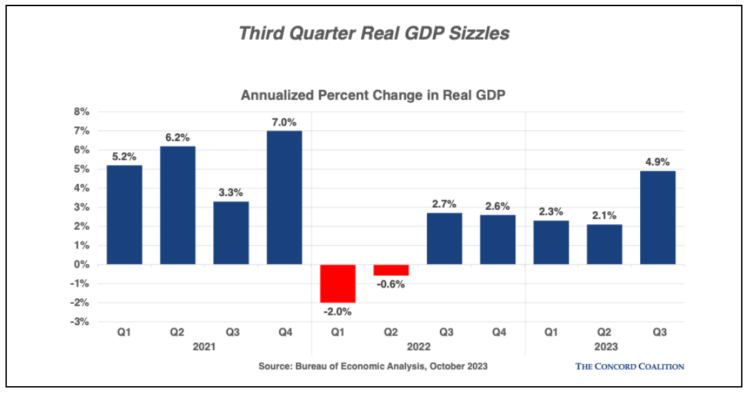

Most economists predicted a strong third quarter real GDP number—consensus estimates ranged from an annualized rate of growth of 4.3 percent (Reuters survey) to 4.5 percent (Bloomberg survey) to 4.7 percent (Dow Jones survey)—a significant acceleration from the second quarter lull of 2.1 percent. The domestic economy over-performed, however, and according to the Bureau of Economic Analysis closed at a sizzling 4.9 percent annualized growth rate.

According to the BEA, “The increase in real GDP reflected increases in consumer spending, private inventory investment, exports, state and local government spending, federal government spending, and residential fixed investment that were partly offset by a decrease in nonresidential fixed investment.”

Growth in consumer spending on goods and services both accelerated in the third quarter (up 4.8 percent and 3.6 percent, respectively), but real disposable personal income contracted by 1 percent, suggesting that this pace of growth is not sustainable. Depleted savings, inflation, and the resumption of student loan payments indicate the U.S. consumer—which makes up two-thirds of the domestic economy—is unlikely to be a powerful growth engine much longer.

Concord’s assessment. When the Federal Reserve meets next to determine future interest rate policy, it will be interesting to learn how the Board processes this GDP estimate in the context of a strong domestic labor market and inflation that has not yet receded to the Fed’s 2 percent target. In recent weeks, yields on the 10-year Treasury note have risen sharply, briefly touching a 16-year high above 5 percent, adding fuel to financial markets’ belief that the Fed will pause another month rather than risk over-correcting. Add to this mixture heightened geopolitical risks in Ukraine and the Middle East and there may be enough uncertainty to compel the Fed to hold rates steady one more month.