Introduction

Earlier this month the Department of Education proposed new regulations to allow more students to avoid repaying the money they borrowed to attend college.[1] These regulations would effectively turn the student loan program into a federal grant for many students and provide substantial subsidies to many other students.

These regulations are the final element in a series of changes announced last year, including $10,000 to $20,000 in debt forgiveness for 43 million students, which is now pending before the Supreme Court, and unlimited debt forgiveness for certain categories of students.[2]

This issue brief will explain the latest proposal, examine its potential impact on the federal budget, and conclude that it exceeds statutory authority and is contrary to congressional intent.

Income-Related Repayment Plans

College graduates typically earn significantly more income throughout their lifetime than non-graduates.[3] The argument for financing their education with student loans is that the additional income allows them to repay their debts. However, not every student earns more, and some fail to graduate, so the cost of a traditional 10-year fixed repayment plan is not always affordable.

To address this concern, Congress and the Department of Education have expanded income-related repayment plans and loan forgiveness programs through legislation and regulation.[4] These plans (which are also called “income-based,” “income-contingent,” or “income-driven”) limit payments based on the borrower’s income and write-off any remaining balance after 20 or 25 years of payments, or even 5 or 10 years if the borrower accepts certain public service jobs.[5]

The Department of Education’s latest proposal would modify one of the existing income-related plans, making it more generous to students and more costly to the government. The key provisions of the proposal would limit loan repayments to 5 percent of the borrower’s income that exceeds 225 percent of the federal poverty guidelines, eliminate the accrual of unpaid interest, and write-off loans up to $12,000 after 10 years of repayments.[6]

The Administration estimates that these changes will cost $138 billion over the next ten years, measured on a net present value basis.[7] However, this estimate assumes the previously announced $10,000 to $20,000 debt forgiveness will be implemented, and therefore only reflects the additional (marginal) cost of these changes. If the Supreme Court strikes down the debt forgiveness plan, the cost of the new proposal would be higher because many students whose debt would have been forgiven will instead participate in the new income-related repayment plan.

The Administration’s estimate also substantially underestimates the likely cost because it assumes the additional subsidies will not result in any additional student loans.[8] To understand why this assumption is untenable, it’s necessary to compare the amount of subsidies and the number of eligible students to those under current law.

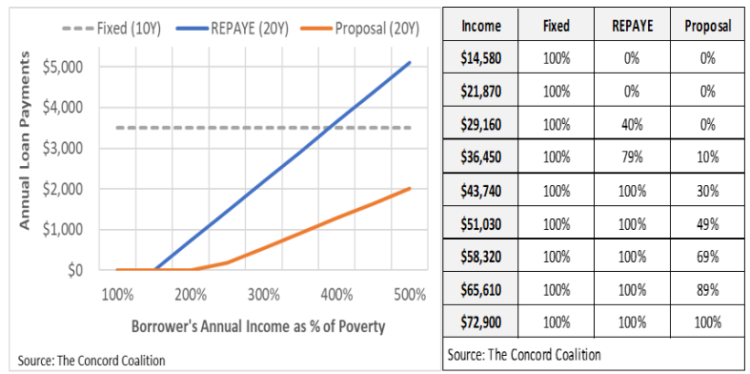

Figure 1 compares the new proposal to the standard repayment plan (Fixed) and the current income-related repayment plan (REPAYE). The current Fixed plan requires equal monthly payments over 10 years, and the current REPAYE plan limits student loan payments to 10 percent of the borrower’s income that exceeds 150 percent of the federal poverty guidelines over 20 years.

The left side of Figure 1 shows how annual loan payments vary with the borrower’s income under each alternative. The right side of Figure 1 shows the present value (PV) of the loan payments required under each alternative as a percent of the original loan amount. Students are assumed to borrow the maximum amount allowed for dependent undergraduates during four years of college ($27,000).[9] The new proposal is substantially more generous than current law. All students earning less than 500% of poverty – or $72,900 a year – would repay less than 100 percent of their loan – in many cases significantly less, or even nothing at all.

Figure 1: Annual Payment and Present Value (PV) of Total Payments as Percent of Loan

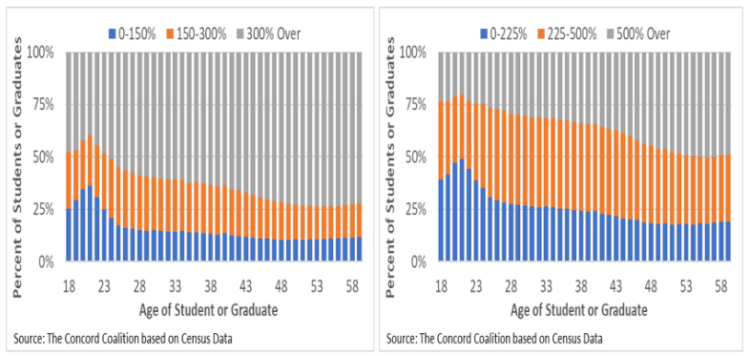

Figure 2 shows the distribution of individuals who attended college and either did not graduate or else received an associate’s (2-Year) or bachelor’s (4-Year) degree by age and income as a percent of poverty. Under the current REPAYE plan, as shown on the left side, roughly 15 percent of students are below 150 percent of poverty (Blue) and would pay nothing, and roughly 22 percent of students are between 150 and 300 percent of poverty (Orange) and would receive a subsidy. Under the new proposal, as shown on the right side, roughly 26 percent of students are below 225 percent of poverty (Blue) and would pay nothing, and roughly 38 percent of students are between 225 and 500 percent of poverty (Orange) and would receive a subsidy. The new proposal would expand the number of individuals eligible to receive a subsidy by 72 percent.[10]

Figure 2: Distribution of Students or Graduates by Age and Income-to-Poverty Ratio

Larger subsidies and expanded eligibility will increase the number of students who choose to fund their education with a student loan. Assuming students eligible to receive a subsidy (as shown in Figure 2) borrowed $27,000 (as shown in Figure 1), the current REPAYE plan would cost the government about $0.20 for every $1.00 of loans, whereas the new proposal would cost $0.43 for every $1.00 of loans. Both figures are measured on a present value basis. The difference is even greater considering the current REPAYE plan would subsidize only about one-third of the students in this scenario, whereas the new proposal would subsidize more than half.[11]

Estimating the cost of the new proposal requires a microsimulation model with longitudinal household income data, like the one developed by the Congressional Budget Office (CBO).[12] Hopefully, CBO will provide their estimate soon. An analysis of an earlier version of the proposal by the Penn-Wharton Budget Model estimated the cost could exceed $450 billion.[13] Given the gap between the amount borrowed and the amount that could be borrowed, the cost will be substantial.

For example, among undergraduates in 2015-2016 (the latest data available), about 7 million students borrowed about $59 billion.[14] If every undergraduate (19 million) had borrowed the maximum amount, the total would have ranged between $130 billion and $217 billion, depending on how many qualified as independent students (e.g., age 24 or older, married, served in the military, etc.).[15]

Despite the difficulty in predicting exactly how much more students will borrow in response to the additional subsidies offered by the new proposal, it should be obvious the number is much larger than the Administration’s estimate of zero.

Yes It’s Expensive, and It’s Probably Illegal

As The Concord Coalition noted in a previous issue brief, the Department of Education’s new proposal likely exceeds statutory authority and is contrary to congressional intent.[16] This conclusion rests on the fact that the original statutory language, which allowed the Secretary to determine how much student loan payments could vary with respect to income, has been limited by subsequent statutory changes.

Income-related repayment plans were enacted as part of a major expansion of the direct lending program included in the Omnibus Budget Reconciliation Act of 1993.[17] The original statutory language gave the Secretary of Education the authority to determine the details of plan, subject to the requirement that the repayment period was “not to exceed 25 years.”

Subsequent statutory changes limited payments to 15 percent of the borrower’s income that exceeded 150 percent of the federal poverty level.[18] Congress subsequently reduced the repayment rate to 10 percent and reduced the repayment period to 20 years.[19]

The Department of Education’s latest plan to use its regulatory authority to reduce the repayment rate to 5 percent, increase the income threshold to 225 percent of poverty, and forgive loans under $12,000 after 10 years, would ignore the statutory thresholds and contradict congressional intent with respect to maintaining the financial integrity of the student loan program.

Conclusion

Income-related repayment plans were intended to help students repay their loans and avoid excessive taxpayer subsidies. These goals are accomplished by limiting loan payments as a share of income and extending the length of the loan. By reducing payments when students have lower income, these plans make college more affordable. By increasing payments when students have higher income and extending the repayment period to 20 (or 25) years, these plans collect additional interest payments without exceeding the present value of the loan, protecting both students and taxpayers.

The new proposal would make college more affordable by allowing students to avoid repaying some or all of their loans. The Department of Education claims “taxpayers would benefit from lower rates of delinquent/defaulted loans.” But writing-off debt to avoid default is like raising the speed limit to prevent speeding tickets. By collecting less than the present value of the original loan, the new proposal shifts the cost of college from students to taxpayers. This shift likely exceeds statutory authority and is contrary to congressional intent. But the question remains, will anyone successfully challenge these actions, or will we see another substantial increase in the national debt as a result of turning loans into grants through administrative action?

[2] Canceling Student Debt: Presidential Power of the Purse? | Concord Coalition; The Biden Administration Takes Another Step Towards ‘Free’ College | Concord Coalition

[3] Do the Benefits of College Still Outweigh the Costs? | (newyorkfed.org)

[4] Income-Driven Repayment Plans for Student Loans: Budgetary Costs and Policy Options | (cbo.gov)

[5] Federal Student Loan Forgiveness and Loan Repayment Programs | (congress.gov); Consolidated loans can be repaid over 30 years.

[6] Poverty Guidelines | ASPE (hhs.gov)

[7] Regulations.gov

[8] Ibid, (p.1919) “The budget estimates assume that there will be no change in volume or quantity of loans issued due to the improved terms. Additional borrowing would likely increase costs of the regulations, but the magnitude of the impact would depend on the characteristics of those borrowing more and data limitations make it challenging to anticipate who such borrowers would be.”

[9] Direct Loan Periods and Amounts | 2022-2023 Federal Student Aid Handbook; Interest Rates for Direct Loans First Disbursed Between July 1, 2022 and June 30, 2023 | Knowledge Center PV = FV/(1+r)^n, where FV is the future value, r is the interest rate, and n is the number of years from the present to the future. The present value calculations assume a 5% interest rate and a 2% inflation rate to adjust annual income and federal poverty thresholds.

[10] (26%+38%) / (15%+22%) = 172%

[11] The Concord Coalition’s analysis of Census data. On average, students would repay $0.80 or $0.57 of the present value of their loan. CBO estimated current IDR plans have a present value cost of $0.17 per $1.00 of loans. Income-Driven Repayment Plans for Student Loans: Budgetary Costs and Policy Options (cbo.gov)

[12] Income-Driven Repayment Plans for Student Loans: Working Paper 2020-02 | (cbo.gov)

[13] The Biden Student Loan Forgiveness Plan: Budgetary Costs and Distributional Impact | (upenn.edu)

[14] Digest of Education Statistics-Most Current Digest Tables, (Tables 331.10, 331.40, 331.45) The total includes federal PLUS loans that parents take out on behalf of their children.

[15] Dependency Status | Federal Student Aid; Maximum for dependent students: Year 1 = $5,500, Year 2 = $6,500. Year 3 = $7,500, Year 4 = $7,500. Maximum for independent students: Year 1 = $9,500, Year 2 = $10,500. Year 3 = $12,500, Year 4 = $12,500.

[16] Canceling Student Debt: Presidential Power of the Purse? | Concord Coalition

[17] Public Law 103-66, STATUTE107.pdf (congress.gov)

[18] Public Law 110-84, PUBL084.110 (congress.gov)

[19] Public Law 111-152, PUBL152.PS (congress.gov)

Download as PDF: Biden Administration is Turning Student Loans into Grants

Continue Reading