It’s been a busy week for budget news: The Congressional Budget Office (CBO) released a preliminary estimate of the budget deficit for FY 2022; the Social Security Administration (SSA) announced a new cost-of-living-adjustment (COLA) for beneficiaries in 2023; and the Bureau of Labor Statistics announced that September core inflation showed no sign of moderating.

The Federal Budget Deficit is Still Too Big

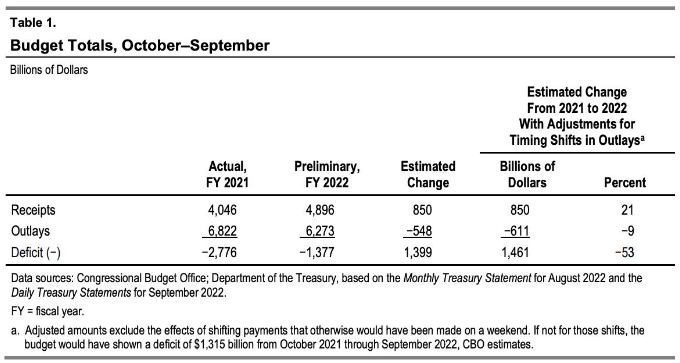

As federal government accountants work to close the books on FY 2022 (which ended September 30), the non-partisan CBO published its preliminary assessment for the just-finished fiscal year. According to their arithmetic, the annual budget deficit fell by nearly half—from $2.8 trillion in FY 2021 to $1.4 trillion in FY 2022—thanks in large part to the end of most COVID-related emergency spending and a big jump in tax revenues attributable to the rapid post-pandemic economic recovery.

To be clear, the decline in the FY 2022 deficit was not the result of affirmative action by Congress or the Biden Administration. Any back-slapping among lawmakers is purely opportunistic. Rather, it was inaction by lawmakers that allowed pandemic-era programs to expire (appropriately). Moreover, the preliminary deficit for FY 2022 is still very high by historical standards (approximately 5.5% of GDP compared to the long-term average of 3.5%) and long-standing underlying trends such as our aging population, excess cost growth in health care, and lackluster labor force growth will propel future budget deficits to unsustainable levels.

Outlays in FY 2022. The federal government spent approximately $6.3 trillion in FY 2022, nearly $550 billion (or 8%) less than the year before. A big decline in outlays attributable to the end of recovery rebates, enhanced pandemic unemployment insurance, the Paycheck Protection Program, and other COVID-related emergency spending meant spending reverted, in large part, to trend this year (2022 outlays more closely resembled pre-pandemic years). These numbers, however, reflect two idiosyncrasies. First, outlays in FY 2022 were affected by a timing shift in the government’s own “pay by” date. Approximately $60 billion in obligations normally due on October 1, 2022 (the start of FY 2023)—were pushed back into FY 2022 because October 1 fell on a weekend.

Second, the budgetary effects of a portion of President Biden’s executive action on student loan debt relief were recorded in FY 2022. According to the Federal Credit Reform Act (FCRA), the costs associated with loan and loan subsidy programs (and any changes to those programs) are estimated on a net present value basis. According to FCRA, the net present value of those amounts, discounted to reflect inflation and other economic risks, is recorded up front in year 1. Since Biden announced his student loan debt forgiveness plan in August, the costs of that plan were booked in FY 2022, adding over $420 billion to the 2022 tally of outlays. [Note: the costs associated with the revised income-driven repayment plan—the second prong in Biden’s two-pronged policy announcement—will be recognized in the year in which the program is finalized (most likely FY 2023).

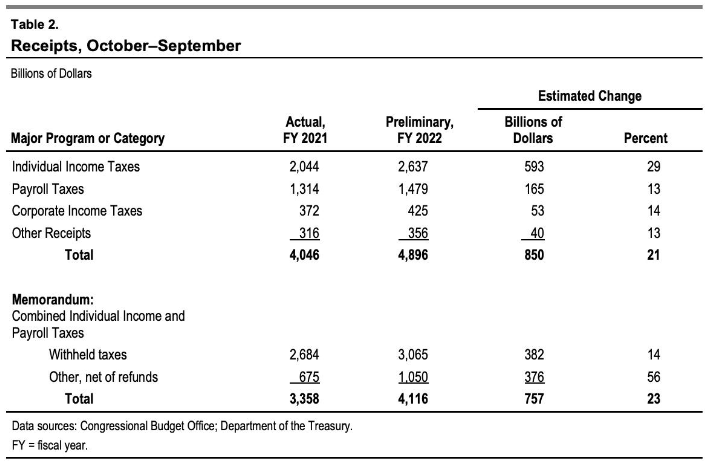

Revenues in FY 2022. Over-performance in revenues across all categories also helped reduce the budget deficit in FY 2022. Revenues totaled nearly $4.9 trillion, $850 billion (or 21%) higher than the prior year. Larger paychecks and the repayment of taxes deferred in 2020 and 2021 led to big gains in individual income taxes (up nearly $600 billion or 29% over FY 2021).

The CBO year-end analysis also reveals that inflation is already having an impact on interest costs to the federal government. Net outlays for interest on the public debt increased by $121 billion (or 29%) in FY 2022, primarily because higher inflation this year has resulted in large adjustments to the principal of inflation protected securities (TIPS). And this is just the beginning…

Social Security Beneficiaries Will Receive Big Increase

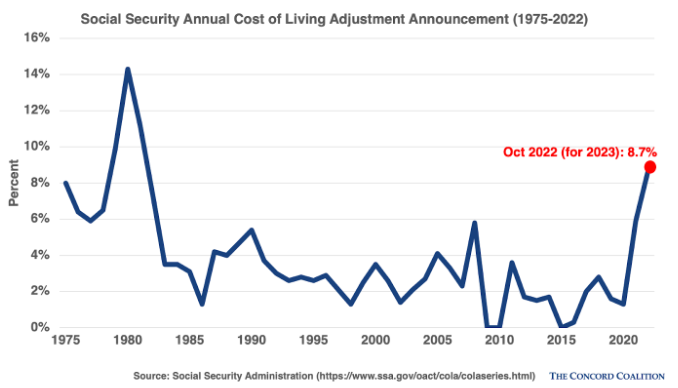

This week, the SSA announced that beneficiaries will receive an 8.7% cost of living adjustment (COLA) increase in their benefit checks in calendar year 2023—the biggest percentage jump since 1981. The increase is based on the level of inflation measured by the Consumer Price Index between the third quarter of 2021 and the third quarter of 2022.

The new COLA will put an additional $144 in the average beneficiary’s check each month—some much-needed help for people on fixed incomes during this period of high inflation. But while this is good news for most recipients, it is bad news for the federal budget. This year, both CBO and the actuaries for the SSA predicted much smaller COLAs for 2023—6.0% and 3.8%, respectively. The higher COLA means outlays for the Social Security program will be approximately $33 billion higher in 2023 than what CBO originally estimated—and that increase will filter through all subsequent years because future COLAs will be added to a now-higher base benefit.

Inflation Shows Few Signs of Abating

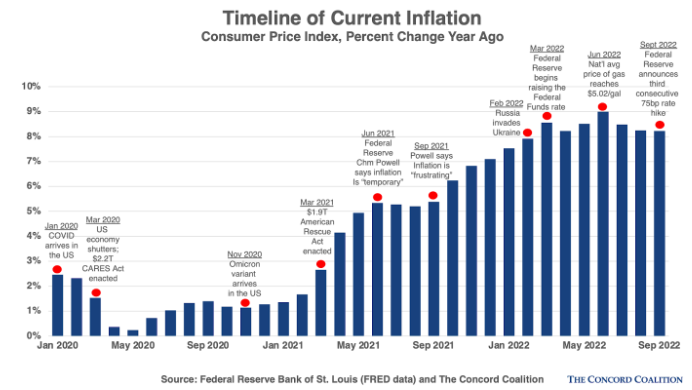

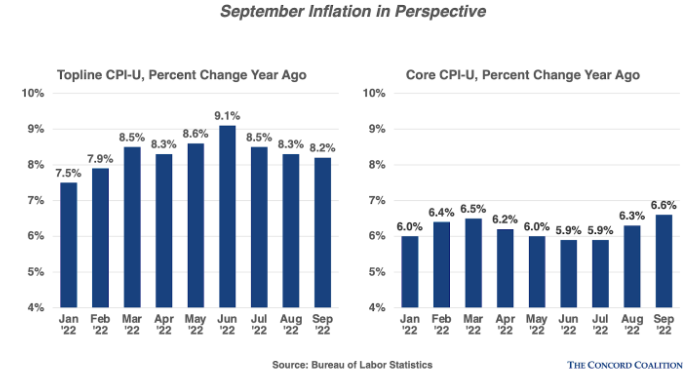

This week, the Bureau of Labor Statistics released its inflation report for September. Bad news: inflation is still too high. Topline inflation registered 8.2% when compared to prices a year ago—a far cry from the Fed’s target of 2%. While September inflation was slightly below the August level, it benefitted from month-to-month price declines in the energy sector—prices which are poised to rise again given the recent decision by OPEC+ member nations to cut oil production by 2 million barrels per day.

More alarming, however, core inflation (which excludes the volatile food and energy categories) was up 6.6% over the same period last year—it’s highest level since 1982—indicating just how firmly inflation has taken root in the consumer economy.

While inflation tends to have similar effects on spending and revenue in the federal budget (both tend to rise with inflation, resulting in little to no change in the primary budget deficit), it can have a significant impact on the interest costs required to service the nation’s $31 trillion federal debt. As inflation rises, investors demand higher interest rates on Treasury securities (because inflation erodes the value of money over time, and investors want to be compensated for that loss with higher interest rates). Already the yield on 10-year Treasury bonds is hovering around 3.9%, approximately one full percentage point higher than what CBO projected in their “Budget and Economic Outlook” earlier this year.

September marked the sixth month in a row that the Federal Reserve raised the Federal Funds Rate to fight inflation and the third month in a row that it raised that target interest rate by 75 basis point, yet core inflation just hit a 40-year high. The effects of monetary policy always lag, but the September inflation report suggests the Fed may need to consider larger rate hikes in the near future if inflation doesn’t show signs of moderating soon.