On March 11, President Biden transmitted to Congress his proposed budget for FY 2025. Although a Republican-controlled House means the Biden budget has little chance of enactment without significant modification, it represents an important starting point for negotiations and is an opportunity to initiate a national dialogue on our policy priorities: what do we want the federal government to provide and how do we want to pay for it?

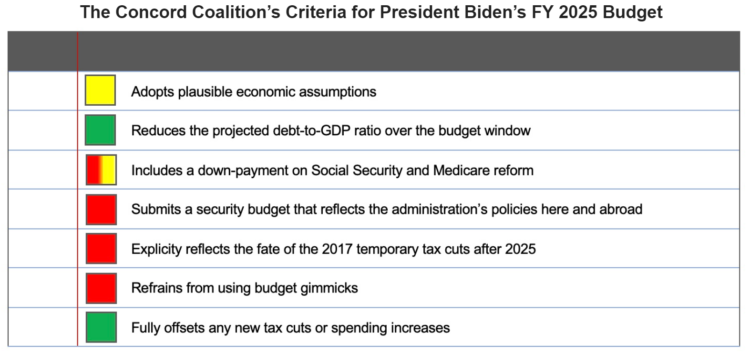

The Concord Coalition developed a list of criteria used to evaluate the President’s new budget. Below is our assessment, color-coordinated like a traffic light: green means “GO” (criteria achieved), red means “STOP” (criteria not met), and yellow means “CAUTION” (some progress achieved).

Adopts plausible economic assumptions

Color code: Yellow

The Administration’s economic assumptions are roughly consistent with other independent estimates prepared at the same time, although slightly more optimistic in terms of long-term economic growth (Table 2-3). However, the greatest economic risk to the budget is the uncertain outlook for inflation and interest rates. The Administration assumes the inflation rate will achieve a level consistent with the Federal Reserve’s 2 percent inflation target (PCE) after 2024, and both short and long-term interest rates will fall below 4 percent after 2025. There is some risk that inflation and interest rates will remain higher than the Administration assumes. A sustained one percentage point increase in both inflation and interest rates would add $2.9 trillion to the national debt over 10 years (Table 2-4).

Reduces the projected debt-to-GDP ratio over the budget window

Color code: Green

In the baseline prepared by the president’s Office of Management and Budget (OMB), debt held by the public reaches 113.3 percent of GDP in 2034. This is slightly more optimistic than CBO’s February 2024 baseline projection where debt held by the public reaches 116 percent of GDP in 2034. In the president’s budget, debt held by the public is 105.6 percent of GDP in 2034. This reduction from the baseline satisfies the criteria, but a few caveats are worth noting. First, although a debt-to-GDP ratio of 105.6 percent in 2034 would be an improvement from the baseline, it would be an increase over the 2023 level (97.3 percent of GDP) and would be just short of the record high (106.1 percent of GDP in 1946). Moreover, the cost of servicing the debt more than doubles between 2023 and 2034 in dollar terms and reaches a record high as a percentage of GDP (3.3 percent) in 2025. It is an indication of how deep and entrenched budget deficits have become that a deficit reduction plan of $3.2 trillion (as proposed in the budget) still leaves debt held by the public and interest costs at such high levels. Stabilizing the debt-to-GDP ratio at today’s level would require a 10-year deficit reduction plan of roughly $6 trillion (plus interest savings), roughly twice the president’s proposal. A deficit reduction plan of that size does not seem plausible at this time, but it shows that the president’s plan, even if enacted, would leave a lot more work to do.

Includes a down-payment on Social Security and Medicare reform

Color code: Social Security Red; Medicare Yellow

The Social Security and Medicare Part A trust funds are projected to be insolvent by 2033, or shortly thereafter. After that date, under current law beneficiaries and providers will no longer be paid in full or on time, effectively reducing their benefits by 21 percent and 11 percent, respectively. The Administration’s budget fails to address Social Security insolvency and includes a mix of policy and accounting changes to address Medicare insolvency. The budget assumes the Medicare payroll tax and the net investment income tax (NIIT) will be increased to 5 percent for taxpayers earning over $400,000, and these rates will also be applied to pass-through businesses. The additional revenue from the higher rates as well as existing revenue from the current rates will both be credited to the Part A trust fund. The Administration’s budget also assumes the savings from its drug price negotiations and drug inflation rebates will be credited to the Part A trust fund. In total, the budget would credit an additional $1.5 trillion to the Part A trust fund, but only $797 billion is due to new taxes. The remainder is an intra-governmental transfer, representing existing taxes already assumed in the baseline, or double-counting prescription drug savings to both offset other spending in the budget as well as extend the life of the Part A trust fund.

Submits a security budget that reflects the Administration’s policies here and abroad

Color code: Red

Since October 2023, Congress and President Biden have been locked in a bitter battle over security and humanitarian aid deemed essential to current epicenters of domestic and international crises: Ukraine, Israel, Gaza, Taiwan and the U.S. southern border. President Biden’s initial $106 billion request to Congress was pared to $95 billion by the Senate and sent to the House for consideration, but House Speaker Johnson has not yet announced any plans to consider the measure.

In his 2025 budget, President Biden renews his call for Congress to pass his original emergency supplemental, but skimps on funding beyond this amount, which suggests that these crises will continue to be paid for with one-off emergency supplemental requests (akin to the wars the U.S. fought in Iraq and Afghanistan). In essence, President Biden’s budget is signaling that the Administration’s policies in these arenas will simply be paid for with more debt–debt that is not reflected in his budget documents.

Crises like these are impossible to predict, but once engaged, the U.S. government needs to do a better job of budgeting for our commitments including promises to foreign allies. The wars in Ukraine and Gaza show no signs of ending soon, and it is wise to assume additional military and humanitarian aid will be required beyond what’s been requested to date. And once the wars end, U.S. foreign policy will shift to reconstruction, opening another necessary spigot of financial aid. It is woefully naive to think these commitments don’t exist in our future, and fiscally irresponsible to fail to budget for them.

Explicitly reflects the fate of the 2017 temporary tax cuts after 2025

Color Code: Red

The president’s revenue baseline assumes the 2017 tax cuts will expire in 2025 as enacted, but his budget also includes a paragraph saying that even though the tax cuts were fiscally irresponsible, President Biden supports extending the tax cuts for taxpayers earning less than $400,000:

President Trump and congressional Republicans deliberately sunset portions of the Tax Cuts and Jobs Act of 2017 legislation after 2025 to conceal both the true increase in the deficit—much larger than the already-massive $2 trillion cost estimate—and the true size of their tax breaks for multi-millionaires and large corporations. This was one of the most egregious and fiscally reckless budget decisions in modern history. The President, faced with this fiscally irresponsible legacy, will work with the Congress to address the 2025 expirations, and focus tax policy on rewarding work not wealth, based on the following guiding principles. The President:

- Opposes increasing taxes on people earning less than $400,000 and supports cutting taxes for working people and families with children to give them more breathing room;

- Opposes tax cuts for the wealthy—either extending tax cuts for the top two percent of Americans earning over $400,000 or bringing back deductions and other tax breaks for these households; and

- Supports paying for extending tax cuts for people earning less than $400,000 with additional reforms to ensure that wealthy people and big corporations pay their fair share, so that the problematic sunsets created by President Trump and congressional Republicans are addressed in a fiscally responsible manner.

—Office of Management and Budget, Budget of the U.S. Government Fiscal Year 2025, p4-476.

This is classic Washington double-speak. The OMB uses the expired tax breaks to inflate the Administration’s revenue projections (thus reducing future deficits) but then claims to support extending most of them. You can’t have it both ways.

Refrains from using budget gimmicks

Color code: Red

It is not unusual for presidential budgets to contain gimmicks that make the proposal appear more fiscally responsible than they really are and President Biden’s FY 2025 budget is no exception (another sad commentary on the state of the Congressional budget process). Two scoring gimmicks have been noted above: (1) Medicare Part A trust fund solvency improvements rely in part on shifting resources from other parts of the budget, and (2) the budget benefits from a revenue boost after 2025 attributable to the expiration of temporary tax cuts that the administration says it wants to extend for most taxpayers.

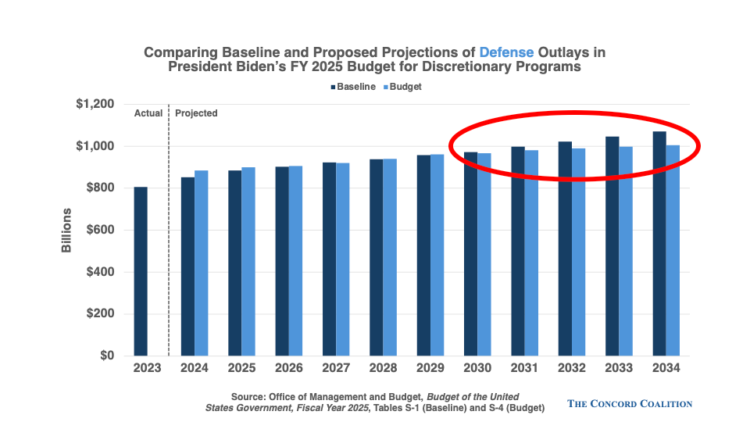

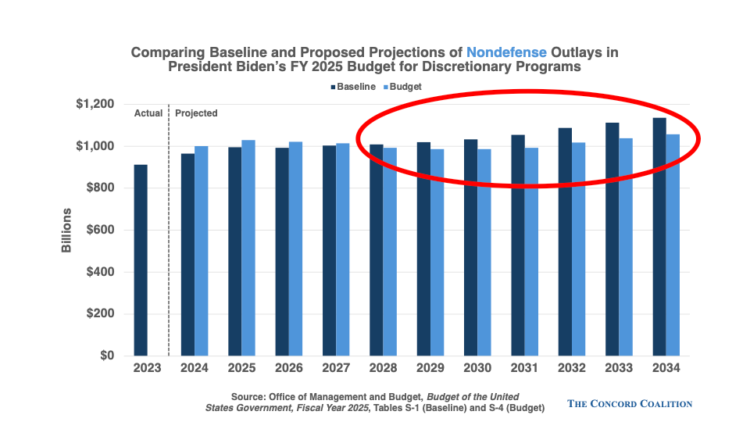

Another scoring gimmick is to assume unrealistic cuts in discretionary spending (defense and non-defense appropriations) in the outyears. For example, President Biden’s budget shows defense outlays rising relative to the baseline through 2029, but reduces defense outlays thereafter. Similarly, non-defense outlays rise relative to the baseline through 2027, but fall thereafter. Inflation and population growth alone make these outyear projections implausible at best, and disingenuous at worst.

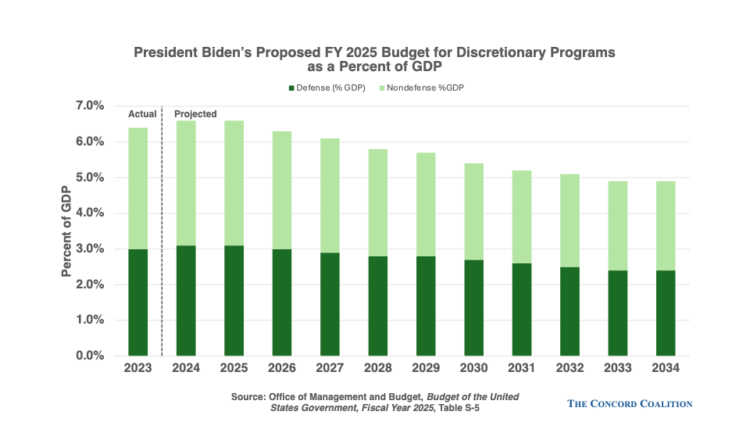

To fully see the fanciful nature of these assumptions, consider the trajectory of defense and non-defense discretionary outlays relative to the size of the economy. In his 2025 budget, President Biden assumes discretionary spending falls from 6.4 percent of GDP in 2023 to 4.8 percent by 2034 even though the administration expects the economy to grow over this period. To put this in context, discretionary outlays have averaged 8.7 percent of GDP over the past 50 years and have never been lower than 6 percent of GDP during this time. In other words, the President’s budget assumes that future lawmakers will make spending cuts that lawmakers, including past presidents, have been unwilling to make.

Fully offsets any new tax cuts or spending increases

Color code: Green

The president’s budget more than pays for the cost of new initiatives. New revenue exceeds new mandatory spending in 2025, as well as over the first five-year period (2025-2029) and over the full 10-year period (2025-2034). While this result satisfies the criteria, it should be noted that total mandatory spending exceeds the baseline by $2.5 trillion over 10 years, swamping the modest discretionary spending savings and substantially eroding the deficit reduction that would otherwise result from the $4.9 trillion proposed revenue increase over 10 years. Digging out of a hole takes a lot longer when you keep adding sand.

Continue Reading